By John Lorinskas

What We’re Hearing and Learning About the Reshoring of the Microchip Industry

Martec President Rick Claar not too long ago wrote about the reshoring trend unfolding currently, exploring what companies can do to pursue such initiatives with confidence and purpose in order to eliminate risk and loss. His piece called to mind the much publicized semiconductor chip shortage that initially emerged during the time of the pandemic.

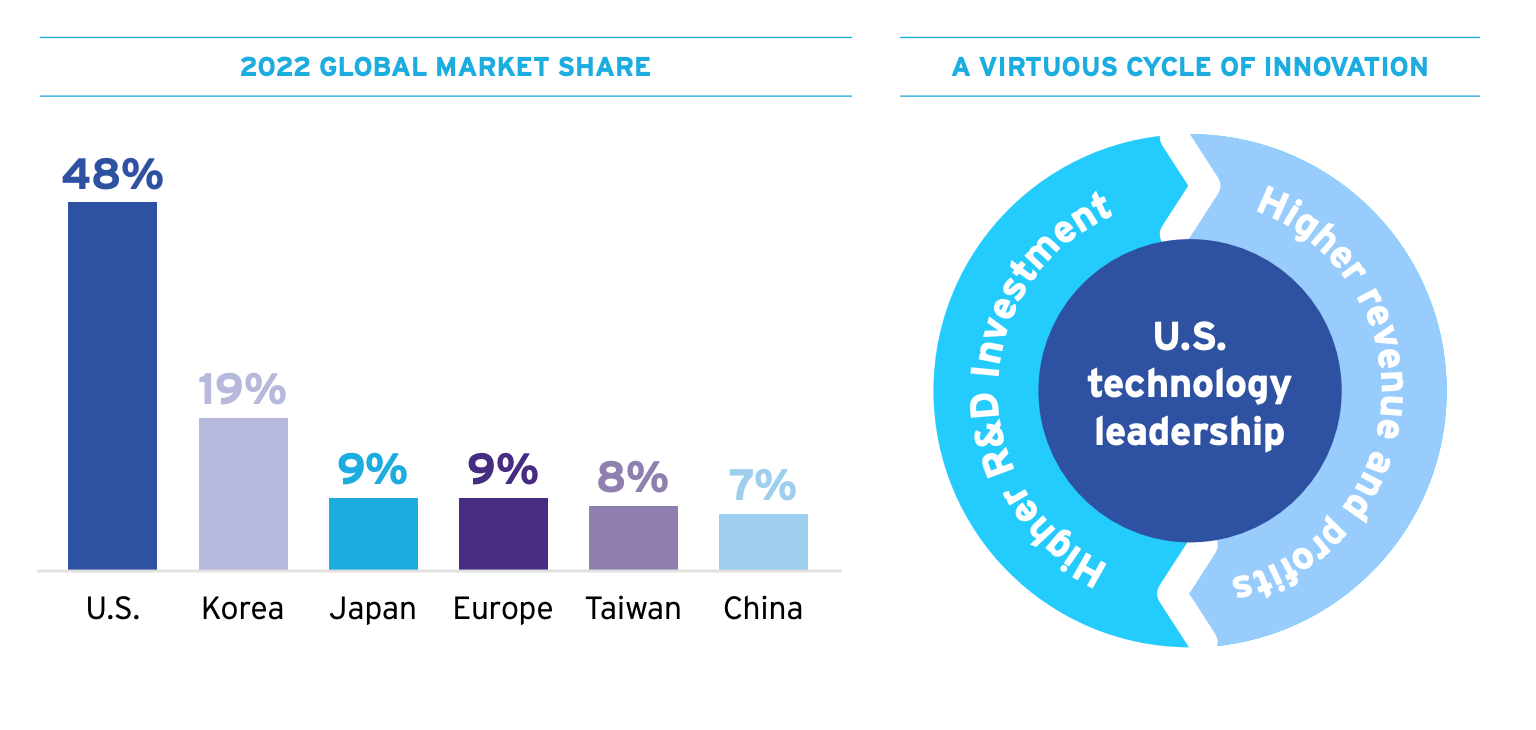

With demand for microprocessor chips escalating, and both the supply chain and raw materials access tightening, global players were understandably concerned about the risk of having roughly 80% of chip manufacturing capacity being located in Asia. Among the myriad new realities presented practically overnight in “the new reality” that COVID brought was a reevaluation of domestic resourcing and supply chain — even to the point of evoking geopolitical and national security considerations.

What naturally followed was a resultant reconsideration of whether American industry should move to quickly and purposefully reshore production of semiconductors — for economic, diplomatic, and even national security reasons.

Just as my colleague Rick pointed out in his thoughtful piece on reshoring, as the pendulum moves in one direction — then back again — there is a lot to examine, research, understand and unpack when making big, bold strategic decisions that can dramatically impact companies and entire sectors. Semiconductor fabrication is no different.

The Ear to the Ground in Semiconductor Fab Trends

The Semiconductor Industry Association recently released its 2023 State of the U.S. Semiconductor Industry report, a thoroughly researched study on current trends and future prognostications from perhaps the authoritative source in the space. It reveals, in part:

As chip demand rises, countries around the world have been ramping up government investments to lure semiconductor production and innovation to their shores. In 2022, the U.S. government stepped up to meet this challenge, enacting the landmark CHIPS and Science Act to provide needed semiconductor research investments and manufacturing incentives. and reinforce America’s economy, national security, and supply chains.

Since the CHIPS Act was introduced, companies from around the world have responded enthusiastically, announcing dozens of new semiconductor ecosystem projects in the U.S. totaling well over $200 billion in private investments. These projects will create tens of thousands of direct jobs in the semiconductor ecosystem and will support hundreds of thousands of additional jobs throughout the U.S. economy.

Although the future holds tremendous promise for the semiconductor industry, it also presents a range of challenges. U.S.-China tensions continue to impact the global supply chain, for example, spurring new government controls on sales of chips to China, the world’s largest semiconductor market. And other significant policy challenges remain, including the need to enact policies to reinforce U.S. leadership in semiconductor design, strengthen the U.S. semiconductor workforce by reforming America’s high-skilled immigration and STEM education systems, and promote free trade and access to global markets. In addition, while the global chip shortage has eased, macroeconomic headwinds and market cyclicality have caused a short-term downturn in sales, which is projected to linger throughout the year.

Bold emphasis is mine in both cases above. You can read the tea leaves for yourself:

While you can download the full report yourself here, two chief takeaways appear to be:

- With great opportunity often comes challenges — some of them hidden and not easily recognizable without careful study.

- Market cyclicality and volatility are important trend lines to pay close attention to, as companies evaluate the above-referenced opportunities and successfully navigate away from the hidden perils.

If the Gold Rush produced the old but oft-referenced trope, “There’s gold in them there hills,” what companies want to know in today’s modern equivalent is:

- Is there “gold” — financial upside and market share to pursue in the domestic semiconductor fab space?

- Which “hills” — where do the opportunities exist, from a vertical and specialization standpoint along the complex supply and production chain in an increasingly diversifying market for semiconductor products, specialists, and infrastructure support, among other interconnected opportunities?

- Where is “there” — where does the greatest opportunity present itself from geographic and economic standpoints, and where are the proverbial land mines and blind spots that should be avoided?

The Rising Tide Lifts Many Boats

The article I mentioned at the outset — Rick Claar’s piece on reshoring — offers the proscriptive advice to “Look Before You Leave.” Rick underscores the importance of carefully examining all relevant considerations before making decisions based on optimism and reasonably informed projections.

Even if prior predictions of a “boom” have moderated in more recent months, as supply catches up to demand, SIA’s own research suggests that the longer trendlines seem to support that “the semiconductor industry’s importance to the world continues to grow, as chips become an even greater presence in the essential technologies of today — and give rise to the transformative technologies of tomorrow.”

Companies and countries around the world experienced firsthand the discomfort that an over-reliance on overseas manufacturing and supply can present to manufacturers, suppliers and retailers across the industrial spectrum.

At the same time, the semiconductor industry has historically been notoriously cyclical. Squeezing global supply has often driven a significant period of growth and capacity expansion, followed by a “bust” cycle where capacity overshoots consumer demand and growth halts while markets grow. While some experts predict that this cyclicality may no longer hold true for the industry, common questions for us as researchers include, “Are we at a good point in the cycle to invest?” or, “Is semiconductor cyclicality finally ending?”. Watching the current trends in semiconductor investment and looking for clues as to its trajectory, as well as advising companies as to the opportunity window for their entry into the market, have been ongoing challenges we have been asked to address.

Whether it’s a boom or something closer to sustained growth and expansion, what is not to be overlooked are the follow-on effects that such trends will surely bring to the fore. It’s not just the semiconductor fabrication industry that will experience growth; it will be the suppliers to these pioneering companies that will see dramatic opportunities as well. From transportation to infrastructure, to materials and service-sector specializations…jobs, investment, construction, development, and everything that goes along with it, will be “following the money” wherever it may lead.

We are already seeing an increase in both the number and the vertical diversity of companies looking for insights, direction, and data-informed analysis to support their forays into these opportunities. They are asking those questions referenced above: Where? When? How? Why? Why not? Who?

To gain that clarity and confidence, there are a variety of disciplines that can be explored to use data and intelligence to drive decision making — whether a company chooses to be a pioneer, an early adopter, or even the late majority and laggards — such as:

- Opportunity Analysis: understanding the market size and totality of opportunity

- Competitive Analysis: learning which of your competitors might be exploring similar opportunities, or researching who existing competitors may be in this new market opportunity you’re exploring

- Industry Trend Analysis: knowing the segment’s Voice of Customer and Voice of Industry to better understand hidden risks and opportunities of entering a “foreign” environment

- M&A Exploration: investigation of supplier acquisition or other “bolt-on” growth opportunities

- Adjacency Investigation: uncovering opportunities to provide “supplemental” support to a growing industry, even if the semiconductor industry is yet foreign to you (e.g., providing infrastructure support or HVAC services to the construction of new plants, as just two examples)

- Geographic Analysis: surveying to identify the likely hubs of activity to bubble up (akin to “Silicon Valley”) to understand where the energy, investment, jobs and opportunities will be flowing

In speaking with real-world companies and professionals working to understand the myriad factors at play during this significant move to reshore the semiconductor industry (government and financial incentives being what they are), we have invested considerable horsepower and energy into understanding the near- and long-term potentialities through secondary research and close study. What we are finding so far is largely supported by SIA’s 2023 report as well.

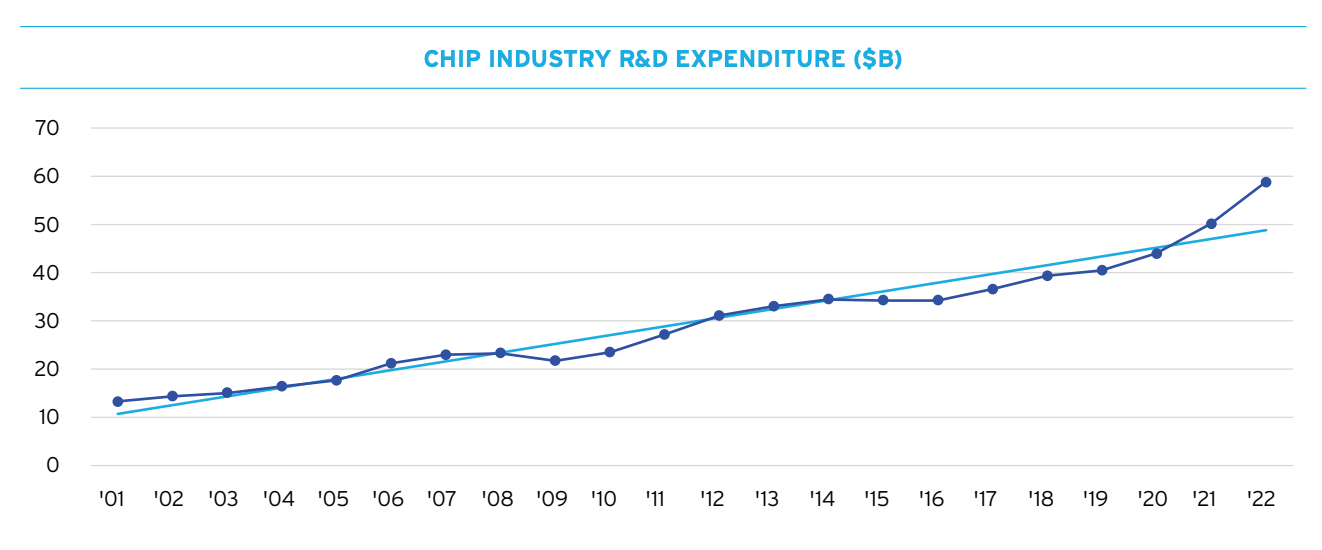

“In 2022, total U.S. semiconductor industry investment in R&D totaled $58.8 billion, a compound annual growth rate of approximately 6.7 percent. R&D expenditures by U.S. semiconductor firms tend to be consistently high, regardless of cycles in annual sales, which reflects the importance of investing in R&D to semiconductor production.”

If recent past is prologue, the future is bright, but not blinding…if you know where to look.

John Lorinskas serves as project manager for Martec. Contact him at john.lorinskas@martegroup.com for questions about reshoring research or any of the disciplines referenced throughout this article..